diminished value claim oregon: Expert Guide to Recovery

"I was satisfied once John Bell took over my case."

"Communication was always timely."

diminished value claim oregon: Expert Guide to Recovery

So, you’ve been in a car accident. Even after the best body shop in town works its magic, your car just isn’t worth what it used to be. That drop in market value is a real financial hit, and in Oregon, you have the right to get that money back from the at-fault driver's insurance. This is called a diminished value claim. It's not about paying for the repairs; it’s about compensating you for the permanent black mark on your vehicle's history.

What Is a Diminished Value Claim in Oregon?

Let's put it in real-world terms. Say your pristine SUV was worth $35,000 right before someone rear-ended you. After top-notch repairs, it looks brand new. But now, because of the accident on its record, a potential buyer will only offer $29,000. That $6,000 difference is your diminished value.

It's a tangible loss caused by someone else's mistake, and Oregon law says you can—and should—be compensated for it.

The logic is simple. Given two identical cars, a buyer will always pay less for the one with an accident history. This isn't just a gut feeling; it’s a market reality that shows up on every vehicle history report from services like CarFax or AutoCheck.

Getting a Grip on the Financial Hit

Making a diminished value claim in Oregon is all about being made financially whole again. The other driver's insurance policy is on the hook not just for the bodywork, but for the loss in your car's resale value, too. This is called inherent diminished value—the automatic drop in market value that happens the second an accident is reported.

Think about it this way: a car worth $27,000 before a crash might only fetch $22,000 after repairs. That’s a $5,000 loss you shouldn't have to absorb. A diminished value claim is designed to recover exactly that amount.

A successful claim ensures the other driver's mistake doesn't cost you thousands of dollars down the line when you decide to sell or trade in your vehicle. It's about fairness and accountability.

Why This Matters for Oregon Drivers

A common misconception is that once an insurance company pays for repairs, their job is done. That’s flat-out wrong. Their legal duty is to restore you to the exact financial position you were in moments before the crash. Since repairs alone can’t erase the stigma of an accident history, paying for diminished value is a critical part of making you whole.

This isn’t just for major collisions, either. Even a minor fender-bender can impact your car's value once it's on the record. After all, buyers get nervous about any reported damage, and it’s important to understand the many common culprits that ruin car paint and vehicle condition.

So, what determines the size of your claim? A few key elements come into play.

The table below breaks down the primary elements that determine the potential value of your claim, helping you quickly assess your situation.

Key Factors Influencing Your Oregon Diminished Value Claim

| Vehicle's Age and Mileage | Newer cars with low mileage lose a much higher percentage of their value. | A 1-year-old car with 10,000 miles will have a larger claim than a 7-year-old car with 120,000 miles. |

| Pre-Accident Condition | A car that was in mint condition before the wreck has more value to lose. | A meticulously maintained car will have a higher diminished value than one with prior dings, dents, or rust. |

| Severity of the Damage | Structural or frame damage is a major red flag for buyers and causes the biggest value drops. | Repairs involving frame straightening or airbag deployment will result in a much higher claim than a simple bumper replacement. |

| Market Desirability | High-end, luxury, or popular models often suffer a greater financial hit. | A Tesla or a new Ford Bronco will see a larger percentage drop in value compared to an older, less popular sedan. |

By understanding how these pieces fit together, you can better estimate what your claim might be worth. Knowing the law is on your side is the first step—now you can confidently move forward to get the compensation you're owed.

The Law is on Your Side in Oregon

Filing a diminished value claim in Oregon isn't some clever trick or a legal loophole. It's your right, plain and simple, and it's backed by decades of state law. Knowing this from the start is your biggest advantage, especially when you're up against an insurance adjuster who might try to convince you otherwise.

The whole point of insurance is to make you "whole" again after an accident caused by someone else. This means putting you back in the same financial position you were in just moments before the crash. Just fixing the dents and dings doesn't cut it if your car is now worth thousands less. That's where a diminished value claim comes in.

The Case That Set the Standard

To really get a handle on your rights, we have to look back at Oregon's legal history. The courts here have long understood that even the best body shop in the world can't erase the fact that a car has been in a serious accident.

The foundational case is Dunmire Motor Co. v. Oregon Mutual Fire Insurance Co. This landmark ruling established a powerful precedent. It confirmed that an owner is entitled to compensation for the drop in their car's market value, even after it has been perfectly repaired. The court recognized that the "stigma" of a wreck is a real, measurable financial loss.

So, when you argue that your car's value took a permanent hit, you're not just making a point—you're standing on solid legal ground.

At its core, the legal principle is straightforward: If another driver's mistake reduces your car's resale value, you are legally entitled to be compensated for that specific loss. Oregon law puts the responsibility for paying it squarely on the at-fault driver's insurance.

Who Pays? Filing a Third-Party Claim

In Oregon, this is handled through a third-party diminished value claim. This just means you file your claim directly against the at-fault driver's insurance company. Their liability policy is on the hook for all the damage their driver caused—not just the repair bill, but the loss in your car's market value, too.

It's a common point of confusion, but you don't file this against your own insurance. Your collision coverage is there to get your car repaired, not to cover its lost value. The claim for diminished value is aimed directly at the person who caused the accident.

State Recognition Backs You Up

This isn't just some dusty old case law, either. Oregon's own regulatory bodies officially acknowledge inherent diminished value. The state's support for this principle actually goes all the way back to that 1941 Dunmire case, where the court made it clear that top-notch repairs don't get rid of the drop in market value.

Even the Oregon Insurance Division has pointed out that the negative impact on resale value can't be completely undone by repairs alone. You can find more professional insights about this on resources like IRMI.com.

This official recognition gives your diminished value claim in Oregon serious weight. When an adjuster tries to brush you off, you can confidently point to both well-established legal precedent and the state's own stance on consumer protection. Knowing the law has your back is the best tool you have for getting the fair settlement you deserve.

How Do You Calculate Your Car's Lost Value?

After a wreck, you can bet the at-fault driver's insurance company will come to you with a number for your car's diminished value. But let's be clear: this initial offer is almost never a fair reflection of your actual loss. Insurance companies are in the business of minimizing payouts, and they have their own internal, often flawed, formulas designed to do just that.

One of their favorite tricks is a calculation called the 17-C Formula. This is a notoriously arbitrary method that insurers love because it systematically undervalues what you're owed. It slaps a bunch of modifiers on for mileage and damage severity, ultimately spitting out a number that's just a fraction of your vehicle's true loss in value. Whatever you do, don't accept a settlement based on this formula.

Your goal is to counter their self-serving calculation with a credible, evidence-based figure that shows what you’ve actually lost. The key isn't some online calculator—it's getting a professional, independent appraisal.

Why an Independent Appraisal Is a Must-Have

Sure, a generic online diminished value calculator might give you a ballpark figure, but it won’t stand up to the scrutiny of an insurance adjuster. Those tools are one-size-fits-all; they can't possibly account for the specific details of your situation, like the quality of the repair work or the unique market conditions right here in Oregon.

To build a rock-solid diminished value claim in Oregon, you need an expert in your corner. A licensed, independent appraiser will deliver a detailed, defensible report that becomes your single most powerful piece of evidence. Their assessment isn't just a number; it's a professional opinion backed by real market data and industry expertise.

A professional appraisal report takes your claim from a simple request and turns it into a well-documented, evidence-based demand. It immediately signals to the insurer that you're serious and have done your homework, which completely changes the dynamic of the negotiation.

What a Credible Appraiser Actually Looks For

A real appraisal is much more than just plugging numbers into a spreadsheet. A certified professional conducts a deep-dive analysis of several key factors to pinpoint the exact drop in your car's market value.

First, they’ll do a hands-on inspection of the vehicle to assess:

- Quality of Repairs: The appraiser is trained to spot signs of imperfect work. Think mismatched paint, inconsistent gaps between body panels, or overspray. Even high-quality repairs can be detected by a pro, and they all impact value.

- Severity of Damage: Was there any frame or structural damage? Did the airbags go off? This kind of severe damage causes the biggest drop in value because savvy buyers will always shy away from a car with a history of major repairs.

- Parts Used: Were original equipment manufacturer (OEM) parts used, or did the shop use aftermarket or even salvaged parts? Using non-OEM parts can compromise the vehicle's integrity and definitely hurts its resale value.

But the physical inspection is only half the story. The appraiser then dives into the research, focusing on your specific vehicle within the local market.

The final report will carefully consider:

- Pre-Accident Condition: The appraiser first establishes your car's fair market value moments before the crash, taking into account its condition, trim level, mileage, and any custom features.

- Vehicle Desirability: Lower-mileage vehicles and in-demand models (like luxury brands, trucks, or popular SUVs) tend to suffer a much larger percentage loss in value after an accident.

- Local Market Data: This is crucial. The appraiser analyzes actual sales data for similar vehicles in Oregon, comparing cars with clean histories to those with accident records to find the real-world difference in value.

This comprehensive approach gives you a solid, market-based number for your loss. When you're trying to figure out your diminished value, it’s helpful to understand the different ways a vehicle’s worth can be calculated.

Valuation Methods Compared

| Independent Appraisal | Claimants, Attorneys | Objective, detailed, evidence-based, holds up in negotiations/court. | Requires an upfront investment. |

| Insurer's Formula (e.g., 17-C) | At-Fault Insurance Companies | Free and fast (for the insurer). | Systematically undervalues claims, arbitrary, biased in the insurer's favor. |

| Online Calculators | General Public | Quick, free, gives a rough estimate. | Inaccurate, lacks detail, not accepted as credible evidence by insurers. |

| Dealer Opinions | Car Owners | Can provide a quick opinion. | Often subjective, not a formal report, may have a conflict of interest (wants to buy your car cheap). |

As you can see, investing in a professional appraisal is the only way to get an objective, expert valuation that an insurance company will have a hard time disputing.

To learn more about the broader concepts behind these assessments, you can consult resources on professional automotive valuation services. And while you’re calculating your total losses, our general car accident compensation calculator can help you see the bigger picture of your overall claim.

Ultimately, putting your money down on a professional appraisal is the single best move you can make. It sets the stage for a successful negotiation by replacing the insurer's biased math with a number they can't easily ignore.

Assembling Your Bulletproof Claim Package

Winning a diminished value claim in Oregon isn’t about making passionate arguments—it’s about presenting cold, hard evidence. Your job is to hand the insurance adjuster a claim package so thorough and undeniable that giving you a fair settlement is simply their easiest path forward.

Think of it this way: you're building a case. A flimsy, disorganized stack of papers just invites a lowball offer. A professional, well-documented claim, on the other hand, shows them you mean business and puts you in the driver's seat. Every single document needs to tell a part of the story: your car's fantastic pre-accident condition, the severity of the collision, and the real-world drop in market value it has suffered.

The Foundation: Your Independent Appraisal

I can't stress this enough: a professional appraisal is the absolute cornerstone of your claim. It’s not just your opinion; it’s an expert-backed valuation that gives your demand instant credibility. Make sure the report you get is comprehensive—it should break down the appraiser's methods, the market data they used, and a clear, final number for your loss.

This report should be the very first thing the adjuster sees after your demand letter. It immediately signals that your claim is based on an objective, third-party assessment, not just what you feel the car is worth.

Submitting a claim without a professional appraisal is like going to court without your key witness. It leaves you completely exposed to the insurance company's biased formulas and lowball tactics.

Critical Supporting Documents

With the appraisal as your foundation, it’s time to add the supporting evidence. These documents paint the full picture for the adjuster, validating everything from the crash's severity to your car's pristine condition beforehand.

Here’s what you absolutely need to include:

- The Police Report: This is the official story of what happened. It establishes the facts of the accident and, most importantly, identifies the at-fault driver, which is the entire basis for your claim against their insurance.

- Photos and Videos (Before and After): Visuals are incredibly powerful. If you have any photos showing off your car before the crash, they’re gold. Contrast those with detailed pictures of the damage right after the accident. If you can get photos during the repair process, even better.

- The Final Repair Invoice: This document is much more than a bill. A detailed, itemized invoice shows every single part that was replaced and every hour of labor spent. It becomes undeniable proof of the accident’s severity, especially when it lists structural repairs or the replacement of major components.

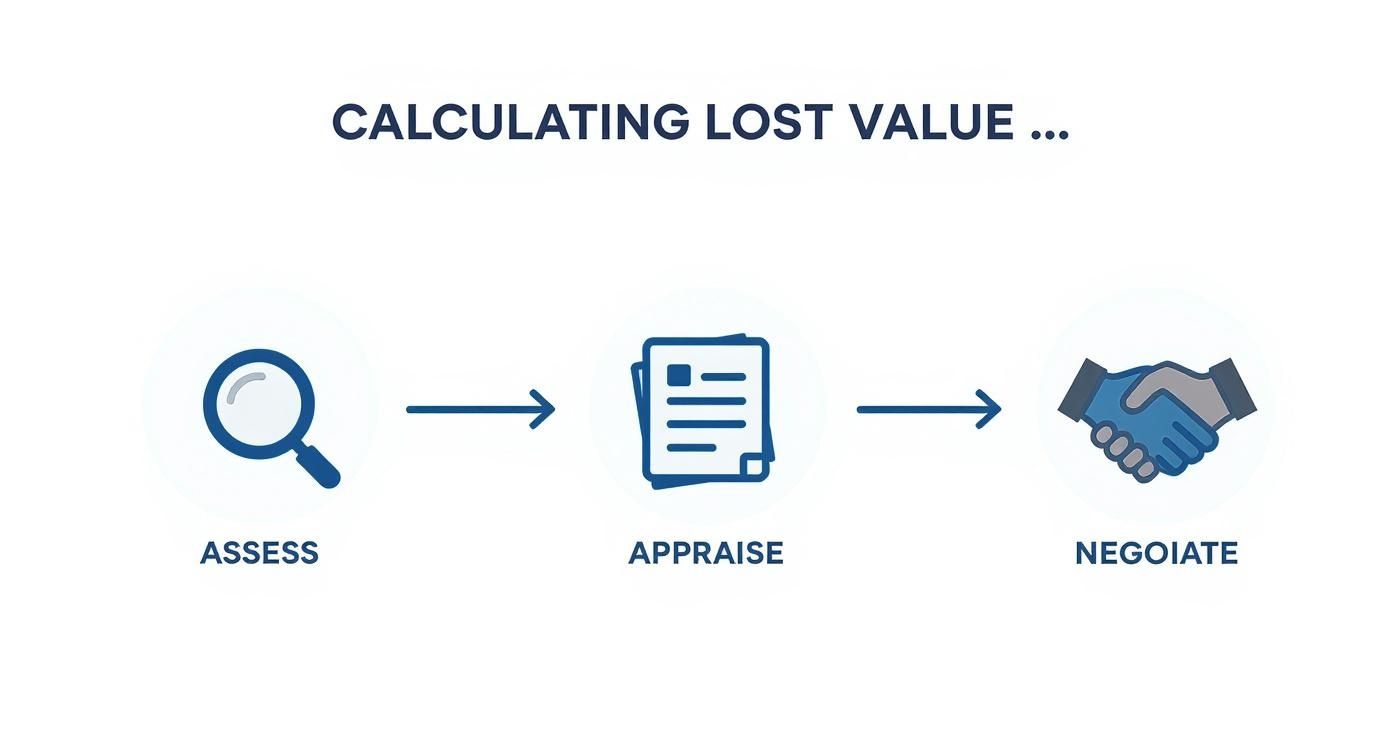

This process—assessment, appraisal, and negotiation—is the core of any successful claim.

As the visual shows, a solid assessment and a professional appraisal are the non-negotiable groundwork for a successful outcome.

Adding Depth with Vehicle History

Finally, you can round out your package with documents that establish your vehicle's history and prove you were a diligent owner. This adds another layer of validation to your appraiser's findings.

Consider including these last few items:

- Vehicle History Report (CarFax/AutoCheck): Here's a pro tip: run this report after the accident has shown up on the record. It provides concrete proof that the collision is now a permanent, value-killing stain on your car's official history.

- Proof of Regular Maintenance: Got service records? Use them. They show you kept the vehicle in top mechanical shape, which justifies its high pre-accident value.

Putting this package together is a huge step, but remember it's just one piece of the post-accident puzzle. To see the full picture, check out our complete guide on what to do after a car accident to make sure you're protecting your rights from day one. When you present a meticulously organized and evidence-rich claim, you fundamentally shift the power dynamic in your favor.

Negotiating a Fair Settlement With the Insurer

You’ve done the hard work of gathering your evidence. Now it’s time to deal with the at-fault driver's insurance company. This is where your careful preparation really shines. Think of this process less as a confrontation and more as a professional presentation of facts. You’re simply showing them the loss and providing the evidence to back it up.

The first step is sending a formal demand letter. This isn’t just a quick email asking for a check. It’s a professional document that lays out the accident details and clearly states your demand for compensation, all based on the diminished value report you secured.

Keep the tone firm but polite. You want to set a professional stage right from the start, showing the adjuster you're organized, serious, and have a rock-solid case.

Crafting a Powerful Demand Letter

Your demand letter is the official starting whistle for negotiations. It needs to be clear and concise, walking the adjuster through your evidence and logically leading them to the same conclusion you've reached: your settlement request is fair.

A strong letter hits all the key points:

- A Clear Introduction: State your name, the date of the accident, the at-fault party's name, and the claim number.

- A Factual Summary: Briefly recount the collision, confirming their insured driver was at fault, and mention that you've included the police report as proof.

- Your Settlement Demand: State the exact dollar amount you are seeking for your car’s diminished value. This number should come directly from your professional appraisal.

- A List of Enclosed Documents: List every piece of evidence you’re providing, like the appraisal, the police report, and the final repair invoice.

When you present a well-organized package, you make the adjuster's job easier. That professionalism can go a long way in shaping the entire negotiation.

Anticipating and Countering Insurer Pushback

Insurance adjusters are trained negotiators, and they have a standard playbook for minimizing what they pay out. Expect a low initial offer. It's not a final "no"—it's an opening move. Being ready for their common arguments is your best defense.

One of the oldest tricks in the book is the claim that "high-quality repairs restored the vehicle to its pre-accident condition and value." We know that's not true. No repair, no matter how expert, can wipe a negative event off a vehicle's history report.

Your counterargument is simple and direct:

"While I appreciate the quality of the repairs, they cannot restore my vehicle's lost market value. The permanent accident history, now documented on services like CarFax, has created an inherent loss that must be compensated for, as supported by Oregon law and the enclosed professional appraisal."

You’ll also likely hear about an internal calculation, often called the 17-C formula. Politely refuse it. State that you can’t accept a calculation based on a biased, insurer-created formula and point them back to your independent, market-based appraisal as the only credible valuation of your loss. For more on this, our guide on how to deal with insurance adjusters provides deeper strategies for these exact conversations.

Standing Your Ground on a Fair Offer

Negotiation is a dance. If the adjuster’s counteroffer is still nowhere near your documented loss, don’t be afraid to hold your ground. Respond in writing, restating your key evidence and calmly explaining why their offer doesn't cover your actual damages.

Remind them of the specific findings in your appraisal. Was there frame damage? Did the airbags deploy? These are massive value-killers that their internal formulas almost always ignore. The goal is to constantly bring the discussion back to your facts, not their opinions.

Nationally, the average diminished value claim is around $1,500, but this figure can be misleading. Individual claims in Oregon can be much higher depending on the vehicle, the extent of the damage, and market realities. In one documented Oregon case, a Mercedes-Benz Sprinter van recovered $6,350 in diminished value because of structural damage and a misleading Carfax report. It’s a perfect example of how the real loss can be substantial.

Knowing Your Deadline: The Statute of Limitations

Time is not on your side forever. In Oregon, the statute of limitations for property damage claims—which includes diminished value—is six years from the date of the accident. While that seems like a long time, don't let it lull you into a false sense of security.

The best strategy is always to file your claim as soon as the repairs are done. The evidence is fresh, your vehicle’s condition is easy to document, and it signals to the insurer that you're on top of things. Waiting years can muddy the waters and make you look less serious about your claim.

Think of the statute of limitations as a final backstop, not a target date. If negotiations hit a wall and you need to file a lawsuit to get what you're owed, you absolutely must do so before that six-year window closes. If you miss it, you forfeit your right to recover anything.

Common Questions About Oregon Diminished Value Claims

Even with the best game plan, you're bound to have questions. Pursuing a diminished value claim in Oregon can feel like navigating a maze, but getting clear on a few key points can really smooth out the path. Let's tackle some of the most common questions we hear from clients.

Can I File a Claim If I Caused the Accident?

This is a big one, but the answer is pretty cut and dried: generally, no. Think of a diminished value claim as a third-party claim. You're filing it against the insurance company of the driver who was at fault for the crash.

Your own collision policy is there to pay for the repairs, getting your car back on the road. It isn't designed to cover the drop in resale value that happens after those repairs are done. To have a valid claim, you need to be the one who wasn't at fault.

Is There a Time Limit to File My Claim in Oregon?

Absolutely, and you don't want to miss this deadline. Oregon's statute of limitations gives you six years from the date of the accident to file a lawsuit for property damage, which includes diminished value.

But here’s my advice: don't wait. The best time to start your claim is right after your vehicle's repairs are finished.

Acting quickly keeps the evidence fresh. It's much easier to prove your car's pre-accident condition, and it shows the insurance company you're serious. Letting years pass by only complicates things and can make it look like your claim isn't a priority.

What Should I Do if the Insurance Company's Offer Is Too Low?

First, don't panic. A lowball offer from an adjuster is often just their opening bid. It's frustrating, but it's part of the game. The key is not to get flustered or feel pressured into taking it.

Your first move is to reject their offer in writing. Keep it professional but firm. Point directly to your independent appraisal and calmly explain why their number doesn't reflect the true market loss. Restate your original demand and make it clear it's based on a real market analysis, not their internal (and often flawed) formula.

If they won't budge or negotiate fairly, you have options. You can file a complaint with the Oregon Division of Financial Regulation or bring in an attorney who knows how to handle these specific claims.

Do I Need a Lawyer to File a Diminished Value Claim?

You're not legally required to have a lawyer for a diminished value claim in Oregon. Plenty of people successfully handle their own claims, especially when they come prepared with a solid appraisal and well-organized evidence.

However, there are times when getting an attorney involved is the smartest move you can make.

- High-Value Claims: If you're dealing with a luxury car, an exotic, or a brand-new model, the potential loss is huge and insurers will fight harder.

- Serious Damage: When the car had significant structural or frame damage, the diminished value is substantial, and these are almost always the most difficult claims to win.

- Difficult Insurers: If the adjuster is ignoring you, using bad-faith tactics, or just flat-out refusing to be reasonable.

In these situations, a lawyer provides the leverage you need to break the logjam. An experienced attorney knows the insurer's playbook and can take over negotiations—or file a lawsuit if that's what it takes to get you paid what you're owed.

Navigating the complexities of a diminished value claim requires expertise and persistence. If you're facing resistance from an insurance company or want to ensure you recover the maximum compensation you deserve, the team at Bell Law is here to help. Contact us today for a consultation to protect your rights and your vehicle's value at https://www.belllawoffices.com.

Disclaimer: The information on this page is provided for general informational purposes only and is not legal advice. Reading this content does not create an attorney-client relationship. For advice about your specific situation, please contact a licensed attorney.