Navigating the Process of Personal Injury Claim

"I was satisfied once John Bell took over my case."

"Communication was always timely."

Navigating the Process of Personal Injury Claim

The journey of a personal injury claim really kicks off the second an accident happens. In those first few moments, your focus should be squarely on two things: your immediate safety and preserving any evidence you can. Things like getting medical care, taking photos of the scene, and making an official report are the bedrock of your entire case.

Your First Moves After an Accident

The minutes and hours right after an injury can be a blur. With adrenaline pumping, it's tough to think straight. But what you do in this critical window can make or break your ability to get fair compensation later on. The goal is to protect both your health and your legal rights by laying a solid foundation for your claim.

Seek Immediate Medical Attention

Your health is, without question, the top priority. Even if you just feel a little sore or shaken up, go see a doctor. Many serious injuries—think whiplash, concussions, or even internal bleeding—don't show obvious symptoms for hours or sometimes days.

Getting a prompt medical evaluation is crucial for two reasons:

- It protects your health. The sooner you get a diagnosis and start treatment, the better your chances are for a full and fast recovery.

- It creates a legal record. When a doctor sees you, they create an official report that connects your injuries directly to the accident. This piece of paper is powerful proof against any argument that your injuries happened later.

If you wait to see a doctor, you’re handing the insurance company an excuse to argue that your injuries weren't that serious or were caused by something else entirely. Don't give them that opening.

Document Everything at the Scene

If you're physically able to, your smartphone is your best friend. Evidence has a way of disappearing fast, so you need to capture the scene exactly as it was. My advice? Take way more photos and videos than you think you need, and get them from every possible angle.

Try to capture these key details:

- The final positions of vehicles and any property damage before anything gets moved.

- Skid marks on the road, debris from the crash, or any hazardous conditions like a wet floor in a slip and fall.

- Any visible injuries you have, like cuts, bruises, or swelling.

- The wider environment—traffic signals, weather conditions, the time of day, and lighting.

This kind of visual evidence tells a story that words just can't. It's an objective, time-stamped record that can be incredibly persuasive down the road.

Key Takeaway: Think of your phone as the most important evidence-gathering tool you have. I've seen cases where a single photo—showing a faded crosswalk line or a broken handrail—made all the difference.

Gather Information and Make an Official Report

While you're still at the scene, swap contact and insurance information with everyone involved. If there were people who saw what happened, politely ask for their names and phone numbers. An unbiased account from a witness can add a ton of credibility to your side of the story.

It’s also vital to get an official report filed. For a car crash, that means calling 911 so the police create a report. If you slip and fall at a business, you need to tell a manager and make sure they fill out an incident report. This formal paperwork locks in a timeline and an official version of the facts.

As you think about what to do next, reaching out to a law firm is often a smart move. It can be helpful to understand the client intake processes used by law firms so you know what to expect from that first call.

Building Your Case: Gathering the Proof You Need

Once you’ve handled the immediate aftermath of an accident, the real work begins. Now, it's less about crisis management and more about methodically building a rock-solid case. This phase is all about gathering every piece of paper, every image, and every record that tells the story of your injury and its impact on your life.

Think of it as constructing a narrative for the insurance company—one supported by undeniable proof.

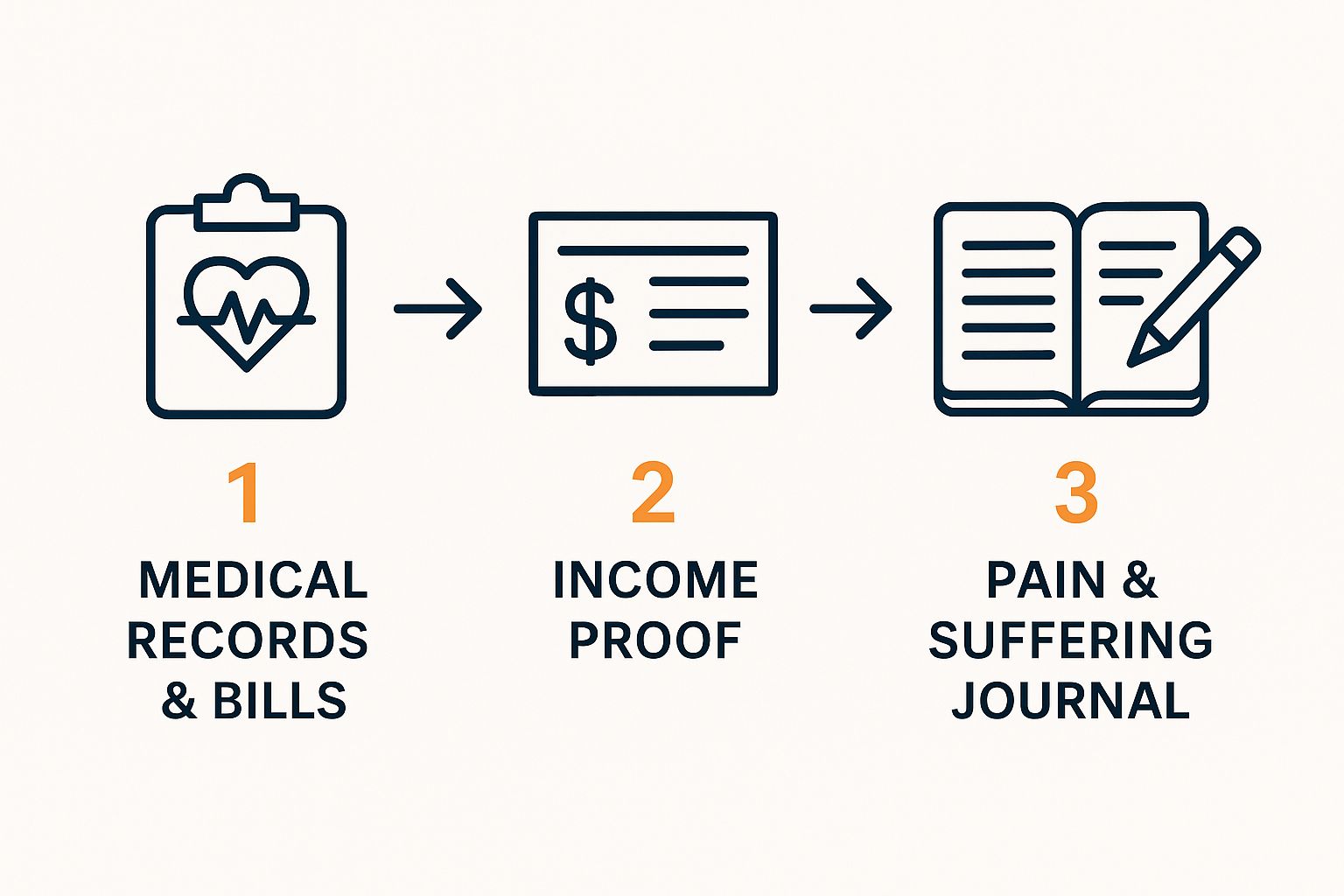

This visual gives you a quick overview of the key evidence pillars you'll be focusing on.

As you can see, your claim rests on weaving together medical, financial, and personal evidence to present a full picture of your damages.

Your Medical Records are the Foundation

The absolute bedrock of any personal injury claim is the medical documentation. Every single doctor's appointment, prescription, and physical therapy session creates a timeline that validates the severity of your injuries. Insurance adjusters live in these records; it's how they gauge a claim's legitimacy.

You need to be a meticulous collector. This includes:

- Hospital and ER records from the initial treatment.

- Bills and itemized statements from every single provider—doctors, surgeons, chiropractors, you name it.

- Objective proof like X-rays, MRIs, and other diagnostic scans.

- Physician’s notes detailing your diagnosis, treatment plan, and long-term prognosis.

Getting all these records can feel like a part-time job, but it's absolutely critical. If you need some help, you can learn more about how to get medical records to make sure nothing gets missed.

Calculating Every Penny of Financial Loss

The financial hit from an injury goes way beyond just the medical bills. You have to prove, down to the dollar, what this accident has cost you in lost income. This isn't about guesswork; it's about presenting concrete evidence.

To prove your lost wages, you'll need:

Pay Stubs: Gather several from before the accident and all of them from after. The difference will paint a very clear picture.

A Letter from Your Employer: Ask your boss or HR for an official letter confirming your job title, your normal rate of pay, and the exact dates you missed work because of the injury.

Tax Returns: Your past tax documents are invaluable for establishing your earning capacity, especially if you're self-employed or your income fluctuates.

This documentation turns a vague claim for "lost income" into a specific, calculated number that the insurance company can't easily dispute.

A Note from Experience: Don't overlook the small stuff. I'm talking about receipts for prescriptions, the cost of gas for driving to and from doctor's appointments, or even a pair of crutches you had to buy. These out-of-pocket costs are part of your economic damages and they add up fast.

Telling the Story of Your Pain and Suffering

This is, without a doubt, the hardest part of a claim to quantify. How do you put a price tag on pain, anxiety, or not being able to enjoy your life like you used to? Your most powerful tool here is surprisingly simple: a journal.

Start writing in it today. Make entries every few days, detailing how you feel—physically and emotionally. Write about the daily struggles. Maybe you couldn't sleep through the night because of the pain, or you had to miss your kid's soccer game.

A journal entry describing how you couldn't lift a grocery bag is infinitely more compelling than simply stating "my shoulder hurts." This personal record adds the human story to your claim, showing the real, day-to-day consequences of the accident.

Mastering The Demand Letter And Negotiations

After painstakingly collecting all your evidence, the case pivots. You're no longer just gathering facts; you're officially making your case for compensation. This crucial transition starts with a single, powerful tool: the demand letter.

This isn't just a simple request for money. Think of it as a formal, professional presentation of your entire case, sent directly to the at-fault party's insurance company. It's where you lay out the indisputable facts, detail the full extent of your injuries, and state the specific, calculated settlement figure you are seeking.

Crafting A Compelling Demand Letter

Your demand letter is your opening argument. It has to be persuasive, crystal clear, and thoroughly supported by the evidence you've worked so hard to compile. A vague or poorly constructed letter sends a signal to the insurance adjuster that you might not be serious, which is an open invitation for a lowball offer.

For instance, let’s say you were in a rear-end collision in Eugene. Your letter wouldn't just say, "The other driver hit me and now my back hurts." It would state the exact date, time, and location, clearly identify the other driver’s negligence (like texting while driving), and cite the police report number as proof.

From there, the letter must weave a clear story of your damages. This means outlining every single medical appointment, from the first trip to the emergency room to your ongoing physical therapy sessions. You'll also provide a detailed accounting of your economic damages—every medical bill, every dollar of lost income, and any other out-of-pocket costs.

Key Elements of a Personal Injury Demand Letter

To make your demand as effective as possible, it must contain several critical components. Each piece works together to build a comprehensive and undeniable picture of your claim for the insurance adjuster.

| Factual Summary | Establishes the undisputed facts of the incident. | "On March 15, 2024, at approximately 2:30 PM, our client was lawfully stopped at a red light... when your insured... violently struck her vehicle from behind." |

| Liability Argument | Clearly states why their insured is legally responsible. | "Under Oregon Revised Statute 811.125, your insured had a duty to maintain a safe following distance, a duty they clearly breached." |

| Detailed Injuries | Documents the full medical scope of the harm caused. | "Ms. Smith was diagnosed with a C5-C6 herniation and post-concussion syndrome, as documented in the attached reports from Dr. Allen." |

| Economic Damages | Provides an itemized list of all financial losses. | "Total medical expenses to date are $14,250.75. Lost wages from her job at XYZ Corp total $5,600." |

| Non-Economic Damages | Explains the human cost: pain, suffering, and life impact. | "The chronic pain from these injuries has prevented Ms. Smith from enjoying her hobbies, such as hiking, and has significantly impacted her quality of life." |

| Settlement Demand | States the specific dollar amount you are seeking. | "Based on the foregoing, we demand a settlement of $95,000 to resolve this claim." |

Ultimately, a well-structured letter backed by solid evidence is your best tool for starting negotiations on the right foot.

The Art Of Negotiation Begins

Once the insurance company gets your demand, the real back-and-forth starts. Be prepared for their first response—it will almost certainly be a lowball offer. This is a standard industry tactic. They're testing you to see if you're desperate enough to accept a quick, cheap payout.

Don't let it discourage you. This is just the opening move. The adjuster might challenge the need for a specific medical procedure or try to argue you were somehow partially at fault. Your job—or your attorney's—is to calmly counter every point with the evidence you've already organized.

Motor vehicle accidents are a huge source of these claims. In the United States, more than 6,500 people are injured in crashes every day, which creates staggering costs from medical bills and lost productivity.

The secret to a strong counter-offer is a methodical response. For every point the adjuster makes, you hit back with a specific piece of proof—a note from your doctor, a statement from a witness, or a photo from the scene. The process of negotiating insurance settlements effectively is a learned skill.

This dance can continue for several rounds. Patience is your most powerful ally. If you want to learn more, our guide on how to negotiate an insurance settlement offers a deeper look at the tactics involved. Every conversation should remain professional and firm, always pushing the settlement number toward a figure that is fair and just.

What Happens When You File a Lawsuit

When the insurance company just won’t budge, filing a lawsuit is the next move. This can sound scary, but let’s be clear: filing suit doesn't mean you’re automatically heading to a courtroom showdown. Far from it.

Think of it as a strategic play. It signals to the insurance company that you're serious and forces them to re-evaluate your claim under the pressure of a formal legal process. More often than not, this is what it takes to bring them back to the table for a real conversation about a fair settlement.

Once the lawsuit is filed, we enter a formal phase of the case called discovery. This is where both sides lay their cards on the table, legally required to share information and evidence. The whole point is to eliminate surprises and give everyone a clear-eyed view of the case's strengths and weaknesses.

Uncovering The Facts During Discovery

Discovery is really just a structured investigation run by the attorneys. It's where the nitty-gritty details of the case get dug up using a few key legal tools.

Here’s what that typically looks like:

- Interrogatories: These are just written questions one side sends to the other. For example, the defense attorney might ask you to list every doctor or physical therapist you've seen since the crash. Your lawyer will be right there with you to make sure your answers are accurate and carefully worded.

- Requests for Production: This is exactly what it sounds like—a formal demand for documents. In a slip-and-fall case, we might request the store’s maintenance logs for the week of the incident or any internal reports about your fall.

- Requests for Admission: These are simple, direct statements that the other side must either admit or deny. We might send something like, "Admit that the driver of your commercial truck was using a mobile device at the time of the collision."

This back-and-forth can unearth crucial evidence that wasn't available before the lawsuit was filed.

Expert Insight: I've seen countless cases turn during discovery. A single document—like a revealing internal email—or a key admission can completely shift the negotiating power and pave the way for a fair settlement without ever setting foot in a courtroom.

The Deposition: Your Sworn Testimony

For most of my clients, the most personal and often nerve-wracking part of discovery is the deposition. A deposition is simply your sworn testimony, given under oath, but it happens in an attorney's conference room, not a courtroom. The other side’s lawyer will ask you questions, and everything you say is recorded by a court reporter. Your attorney will be by your side the entire time.

Imagine you were hurt at work by a piece of malfunctioning equipment. The company's lawyer would want to ask you very detailed questions about your training on that machine, exactly how the accident happened, and all the ways your injuries have impacted your life since. It’s their chance to hear the story directly from you.

These workplace injury cases are unfortunately common. In 2023, the U.S. saw 5,283 fatal work injuries and roughly 2.6 million nonfatal injuries. The economic toll is staggering, reaching $167 billion in 2022 from costs like medical bills and lost wages. You can find more insights on how personal injury law is changing at Sugarman.com.

A huge part of my job is getting you ready for this. We’ll go over what to expect, and I’ll be there to protect you from improper questions and help you tell your story clearly. While it can be intense, a strong deposition shows the other side you are a credible witness, which can dramatically improve your position. It always helps to know how to prepare for a deposition to feel more in control.

Filing a lawsuit and going through discovery are powerful steps. They formalize the fight, force critical information out into the open, and often give the insurance company the push they need to come back to the negotiating table with a realistic settlement offer.

Settlement vs. Trial: The Final Decision

As all the pieces of your personal injury claim come together, you’ll find yourself at a critical fork in the road. One path leads to a settlement—a negotiated agreement that resolves your case for a fixed sum of money. The other path leads to a trial, where the final outcome is placed in the hands of a judge or jury.

It’s crucial to understand the realities of both options to make a smart, strategic decision that's right for you.

The vast majority of personal injury cases never see the inside of a courtroom. It’s a fact that surprises a lot of people, but somewhere between 95% and 96% of these claims are resolved through a settlement. You can dig into more personal injury statistics about settlement rates on CasePeer.com.

This isn't just a coincidence. Settlements offer certainty and control, two things that evaporate the moment you step into a courtroom.

Why Most Cases Settle Out of Court

Settling a case locks in a guaranteed outcome, which is a massive relief for everyone involved. For you, it means you know exactly how much compensation you’ll receive, eliminating the risk of walking away with nothing after a trial.

For the insurance company, a settlement puts a cap on their financial exposure. It also helps them sidestep the staggering costs that come with taking a case all the way through a trial.

Let’s not forget the human element. A settlement avoids the immense stress and emotional toll of a trial. Testifying in open court can be a deeply intimidating experience, forcing you to publicly relive what might have been the worst day of your life. Settling lets you close this chapter privately and put all your energy into your recovery.

The Power of Mediation

Often, the final push toward a settlement happens in a process called mediation. This isn't a courtroom showdown; it's a structured, private negotiation guided by a neutral third party called a mediator.

Here’s a quick rundown of how it works:

- A Neutral Guide: The mediator is typically a retired judge or a seasoned attorney who doesn't take sides. Their one and only job is to help both parties find a path to an agreement.

- Structured Conversation: You and your lawyer will be in one room, while the defense attorney and insurance adjuster are in another. The mediator shuttles between the rooms, relaying offers and giving each side a frank assessment of their case's strengths and weaknesses.

- Completely Confidential: Everything said during mediation stays in mediation. This creates a safe space to talk openly and explore settlement options without worrying that your words could be used against you in court later on.

Mediation is so effective because it compels both sides to take a hard, realistic look at their case and the very real risks of a trial. It’s an incredibly powerful tool for breaking a negotiation stalemate.

From Experience: I've seen mediation work wonders. When both sides are completely dug in and refusing to budge, a skilled mediator can reframe the entire conversation. They can often guide everyone toward a resolution that nobody could see on their own. It’s frequently the last, best chance to settle before committing to a trial.

The Reality of Going to Trial

Deciding to go to trial is a huge step and one that should never be taken lightly. Sometimes it’s the only way to get justice, but it’s always an expensive, time-consuming, and unpredictable journey. The preparation alone is intense, involving everything from witness prep and organizing exhibits to late-night strategy sessions.

The trial itself is a formal, highly structured affair. It kicks off with jury selection, followed by opening statements from each attorney. Then comes the core of the trial: the presentation of evidence, where witnesses are called to the stand for direct questioning and cross-examination. After closing arguments, the case is handed to the jury for deliberation.

This process can last for days, or even weeks. And after all that, there’s absolutely no guarantee of success. A jury could award you less than the insurance company’s final settlement offer—or they could award you nothing at all. This deep-seated uncertainty is the single biggest reason why a fair settlement is so often the most prudent path forward.

Common Questions About Injury Claims

When you're navigating a personal injury claim, it's natural to have a ton of questions. Trying to understand the timeline, figure out what your claim is worth, and decide when to get a lawyer involved can feel overwhelming. Let's walk through some of the most common concerns we hear from our clients every day.

How Long Does a Personal Injury Claim Usually Take?

Honestly, there’s no magic number. The timeline for your claim is completely tied to the unique facts of your case.

A relatively simple claim—say, one where the other party's fault is obvious and your injuries are minor—might be resolved in just a few months.

But if you're dealing with a more complex situation involving serious injuries or a fight over who was at fault, it's not uncommon for a case to take one to three years. This is especially true if a lawsuit becomes necessary, as the process then gets dictated by factors we can't always control.

The biggest things that will influence your timeline are:

- Your Medical Treatment: We can't even think about settling until you've reached what's called "maximum medical improvement." This means you and your doctors have a crystal-clear picture of your long-term prognosis. Settling too early is a massive gamble, as you could leave money on the table for future surgeries or physical therapy.

- The Insurance Company's Attitude: A reasonable insurance adjuster can keep things moving. But an adjuster who drags their feet and uses delay tactics can add months to the process.

- The Court's Schedule: If we have to file a lawsuit, we're at the mercy of the local court's docket. That alone can heavily influence how quickly things move toward trial or settlement.

Rushing an injury claim almost always plays right into the insurance company’s hands. Patience is truly your best asset in making sure you get a settlement that covers everything you need.

How Is the Value of My Claim Determined?

The value of your claim isn't just a number pulled out of thin air. It’s a careful calculation of your “damages”—a legal term for everything you've lost because of the accident. These losses are broken down into two key categories.

First, you have economic damages. These are the straightforward, black-and-white financial losses you can prove with receipts and pay stubs. Think of them as anything you can add up on a calculator, like all your medical bills and every paycheck you missed while out of work.

Second, there are non-economic damages. This is where it gets more complex. These damages are meant to compensate you for the intangible harms: your physical pain, your emotional suffering, and the way the injury has impacted your overall quality of life. An attorney calculates this value by starting with your economic losses and applying a multiplier (usually between 1.5 and 5) that reflects how severe and permanent your injuries are.

Key Insight: The final settlement amount is never a guarantee. It comes down to a negotiation that hinges on the strength of your evidence, the seriousness of your injuries, and the experience of your legal team.

Do I Really Need a Lawyer for My Injury Claim?

You absolutely have the right to handle your own claim, but for anything more than a minor fender-bender, it's a huge risk. Insurance adjusters are trained negotiators. Their entire job is to protect their company's profits by paying you as little as possible. They know the system and all the weak spots to exploit.

Hiring a personal injury attorney levels that playing field. We act as your advocate, and we know the legal tactics adjusters use. We aren't intimidated by lowball offers or the common strategies they use to make you feel like your claim is worth less than it is. An experienced lawyer knows how to properly calculate your total damages, can bring in medical experts to prove your case, and has the resources to go to court if the insurance company refuses to be fair.

Study after study shows that people who hire a lawyer receive significantly higher settlements—often multiple times higher—than those who go it alone, even after you account for attorney fees. If your injuries are serious and will affect your future, getting professional guidance is the best way to protect yourself.

At Bell Law, we've seen firsthand how complex the personal injury process in Oregon can be. If you've been hurt and are unsure about your rights, our team is here to give you clear answers and the support you deserve. Contact us today for a free, no-obligation consultation to discuss your case. Find out more about how we can help at https://www.belllawoffices.com.

Disclaimer: The information on this page is provided for general informational purposes only and is not legal advice. Reading this content does not create an attorney-client relationship. For advice about your specific situation, please contact a licensed attorney.