Oregon Statute of Limitations for Insurance Claims Explained

"I was satisfied once John Bell took over my case."

"Communication was always timely."

Oregon Statute of Limitations for Insurance Claims Explained

When you're dealing with an insurance claim, one of the most critical concepts to understand is the statute of limitations. It can be thought of as a legal deadline that dictates the time limit for filing a lawsuit.

In Oregon, this is not a one-size-fits-all deadline. The timeframe can change based on the type of event—such as a car crash, an on-the-job injury, or damage to property. Gaining a general understanding of this concept early on is an important step in navigating the claims process.

Understanding the Legal Countdown Clock

The idea behind a statute of limitations is to encourage the timely resolution of legal disputes. It promotes bringing claims forward while evidence may still be available and memories are relatively fresh. It also provides a point at which potential defendants may no longer face the possibility of a lawsuit for a past event.

When a car accident or a workplace injury happens, that event is what can start the legal countdown. Every state has its own set of rules for these deadlines, and Oregon is no different. If this time limit expires, a person's right to sue and seek compensation in court could be lost, regardless of the merits of the underlying case.

Why This Deadline Matters

Missing the statute of limitations is a significant issue—it’s not a minor procedural hiccup. It can bar an individual's ability to pursue a legal remedy through the court system. It is also important to know that this legal deadline is separate from the timelines an insurance company may set.

An insurance policy is a contract, and it has its own set of deadlines for things like:

- Reporting the claim: Many policies require policyholders to notify them "promptly" or within a certain number of days.

- Submitting paperwork: There are also often deadlines for sending in a proof of loss form or other required documents.

It is possible to follow every single rule in an insurance policy and still miss the legal deadline to file a lawsuit if a dispute arises. They are two different timelines, and it is helpful to be aware of both.

The core idea behind the statute of limitations is that legal claims should be brought when the facts are relatively fresh. This is intended to support a fairer process by relying on timely evidence and testimony, rather than faded memories and lost documents.

The Purpose of a Legal Time Limit

At its heart, the statute of limitations is about fairness. Consider the difficulty of defending against a claim that happened a decade ago. Witnesses may have moved or become unavailable, evidence could be gone, and memories would be less clear. Setting a timeframe is meant to prevent such situations.

For anyone navigating an insurance claim, just knowing that this time limit exists can be beneficial. It allows a person to formulate questions and be proactive about their next steps.

Navigating Different Claim Deadlines in Oregon

The statute of limitations can be thought of as a legal deadline. However, there isn't just one universal timer for every situation. The deadline for filing an insurance-related lawsuit may depend entirely on what happened.

A personal injury claim from a car crash follows one set of Oregon laws. A workers' compensation claim, on the other hand, operates under a different system with its own reporting timelines. Social Security Disability is a federal program with its own unique deadlines for appeals. Each path has its own framework and its own schedule.

Let's break down some common scenarios to see how different these timelines can be. Understanding these distinctions is a key part of the process.

General Timelines for Common Oregon Insurance-Related Claims

This table gives a quick overview of some general deadlines for different types of claims in Oregon. It is important to remember that these are general guidelines. The specific details of a case can affect the timeline, so this is for informational purposes only.

| Personal Injury (e.g., car accident, slip and fall) | 2 years | The date the injury occurred. |

| Medical Malpractice | 2 years | The date the injury was discovered (or reasonably should have been discovered). |

| Wrongful Death | 3 years | The date of the individual's death. |

| Breach of Contract (e.g., insurance bad faith) | 6 years | The date the contract was allegedly breached. |

As you can see, the starting point and the deadline can vary. This is why it is important to seek clarity on a specific situation as soon as possible.

Timelines for Personal Injury Claims

In Oregon, when an injury occurs due to someone else's negligence—whether in a car accident or a slip and fall—there is generally a specific window to file a lawsuit. Knowing this deadline is important. The ability to file a lawsuit is a factor in settlement negotiations with an insurance company.

This area of law can be complex, and the unique facts of a case can affect how that deadline is calculated. You can learn more by reading our detailed guide on the Oregon personal injury statute of limitations.

Deadlines for Workers Compensation

Workers' compensation is a distinct area of law. It's a separate system from personal injury lawsuits, and the timelines are often much shorter. For instance, an injured worker may have a very limited time to notify their employer about an on-the-job injury.

From there, another deadline may apply for filing the actual claim with the state. These timelines are part of Oregon's workers' comp laws to keep the process moving. Missing one of these early deadlines could impact an individual's ability to receive benefits.

Social Security Disability Timelines

Unlike claims handled at the state level, Social Security Disability (SSD) is a federal program. Here, the critical deadlines are often about navigating the appeals process. If an initial application for benefits is denied—which can happen—an applicant typically has 60 days to file an appeal.

Missing that 60-day window could mean having to start the entire application process over again. This highlights why timely action can be important at every stage of a disability claim.

A statute of limitations is a hard legal deadline. The difference between a two-year personal injury window and a 60-day disability appeal deadline shows why it can be critical to identify the correct timeline for your situation from the start.

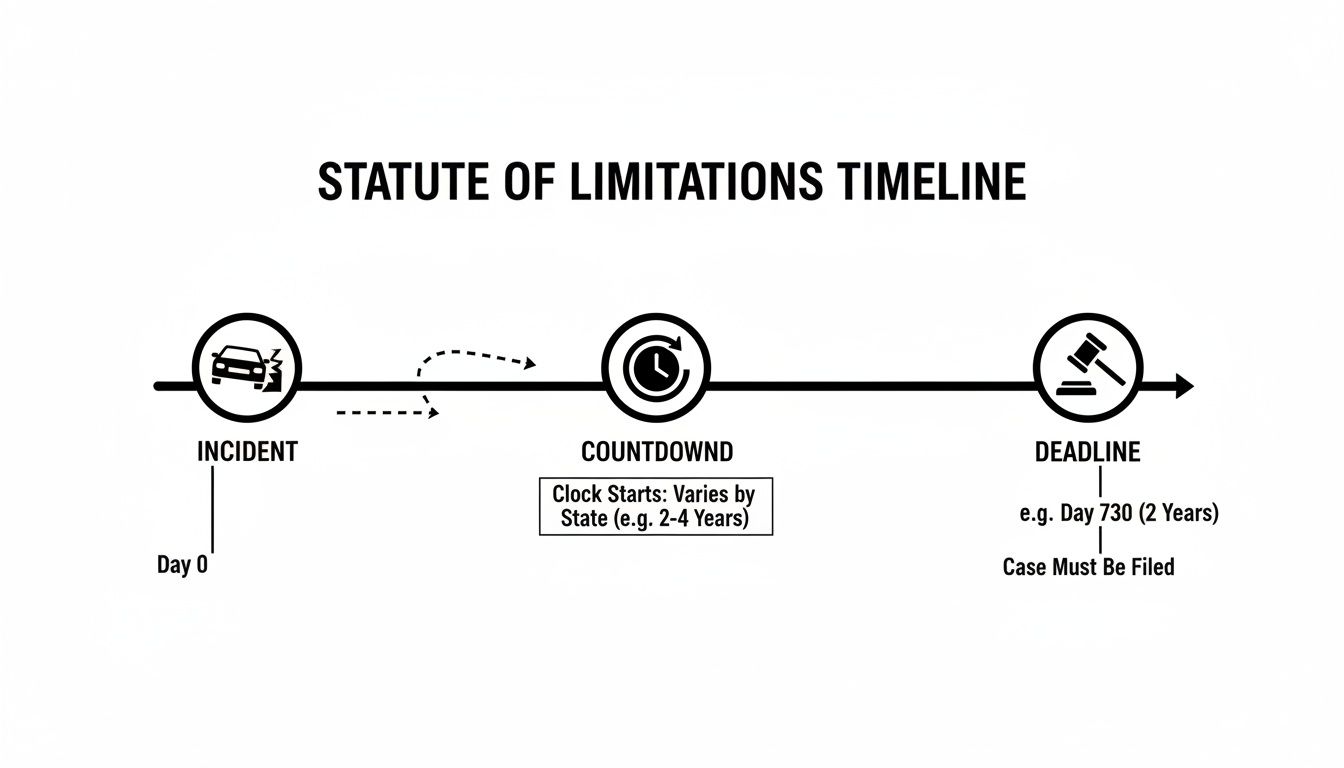

This is a simple way to visualize how that timeline progresses.

The key takeaway? The clock may start ticking the moment an incident happens, not when a person feels ready to take action. Each passing day can be significant.

Why Do These Timelines Vary So Much?

The reason for different rules is that each type of claim serves a different purpose and is built on a different legal foundation. Personal injury law is about holding someone accountable for a "tort," or a civil wrong.

Workers' compensation, however, is an administrative system created as a no-fault framework for workplace injuries. And Social Security Disability is a federal insurance program with its own set of administrative regulations. This kind of legal variety isn’t unique to Oregon; it's how the system works across the country.

Industry data indicates that for many personal injury claims, the statute of limitations is often 2 years. However, this can range from one to three years depending on the state. The rules that apply are dictated by the jurisdiction and the specifics of the case.

When Does the Countdown Clock Actually Start Ticking?

One of the more complex parts of the statute of limitations for insurance claims is figuring out the exact moment the legal clock starts running. A common misconception is that it's always the date of the accident or injury, but in Oregon, the law can be more nuanced.

The official starting point is known as accrual. This is the moment when all the necessary elements of a claim are in place, giving a person the legal right to file a lawsuit. For a straightforward car crash, the "accrual date" is often the day of the accident—the harm is immediate and obvious. But circumstances are not always that simple.

That's where a legal concept called the discovery rule can come into play.

Understanding the Discovery Rule

The discovery rule can be an exception to the standard start date. It’s based on an idea of fairness: a person cannot be expected to file a claim for an injury they do not know they have. The rule states that the statute of limitations clock does not begin until the date an injury was discovered, or reasonably should have been discovered.

Imagine a slow water leak hidden behind a wall. The pipe may have burst weeks ago, but the problem isn't known until a stain spreads across the drywall. The discovery rule can work similarly for injuries that are not immediately apparent.

This rule addresses a fundamental issue: what happens when symptoms are delayed? The law recognizes that a person should not be penalized for not pursuing a claim for an injury they could not have known existed.

This concept can be relevant in several types of cases:

- Medical Malpractice: A surgical error might not cause noticeable pain or complications for months or even years after the procedure.

- Toxic Exposure: Illnesses from being exposed to harmful substances, like asbestos or chemicals, can take a very long time to develop and be properly diagnosed.

- Defective Products: A faulty medical implant could function for a while before it fails and causes harm.

In these situations, the clock might not start on the day of the surgery or exposure. Instead, it could start on the day a doctor connects symptoms to that past event.

What About Breach of Contract Claims?

When a dispute is with the insurance company itself—such as when it denies a claim under the policy—the starting point can be different. For property damage claims, for example, Oregon law may state that the clock starts on the date the loss happened.

This is a critical detail. It means the deadline may be approaching even while negotiations with an insurer are ongoing. For more context on how long an insurance company has to settle a claim, it's helpful to understand the general timelines they are expected to follow.

For a property damage claim, a 6-year clock may begin on the day the damage occurred, not the day the claim was denied. Any delay in the process can affect a person's rights.

Pinpointing the start date is not always black and white. It can depend on the type of claim, Oregon law, and the specific facts of the case. Because this starting point can be a point of debate, it is one of the most important aspects to determine correctly.

Can the Filing Deadline Be Paused or Extended?

While the statute of limitations sets a deadline for insurance claims, it is not always a rigid countdown. There are certain situations where the clock can be paused. This legal concept is called tolling, and it’s designed to address situations where someone cannot reasonably file a claim right away.

Tolling doesn’t reset the clock or erase the time that has already passed. It simply freezes it. The time limit does not run for a period, and then it resumes.

How Tolling Pauses the Legal Clock

So, what kind of situations can pause the deadline?

One of the most common reasons involves the claimant's age. If the injured person is under 18 at the time of the incident, the law recognizes they are not in a position to make complex legal decisions for themselves. In Oregon, the clock for many claims may be paused until they turn 18. Once they become a legal adult, the standard time limit begins to run.

Other situations where a deadline might be tolled include:

- Mental Incapacity: If the injured person is deemed legally incapable of managing their affairs.

- Defendant Flees: If the person responsible for the harm leaves Oregon to avoid being served with a lawsuit, the clock can be paused until they return.

Tolling is a protective measure within the law. It’s a recognition that strict, unbending deadlines could be unfair to people who, through no fault of their own, are legally unable to pursue their rights.

Preventing an Unfair Defense with Equitable Estoppel

Beyond tolling, another legal concept can come into play: equitable estoppel. This is not about pausing the clock but about preventing a defendant from using the deadline as a defense in an unfair manner. It may apply when the actions of the insurance company or at-fault party mislead a person into missing the filing deadline.

For example, if an insurance adjuster makes repeated promises that a fair settlement is forthcoming, and advises a person not to hire a lawyer or file a lawsuit, and that person relies on those reassurances, equitable estoppel might prevent the insurer from later using the statute of limitations as a defense.

To use this doctrine, a claimant generally has to show:

- The insurance company made a misleading statement or took a misleading action.

- The claimant reasonably relied on that statement or action.

- That reliance directly caused the claimant to miss the statute of limitations.

When a Deadline Might Be Extended

In some situations, like those involving wrongful death, the law sets out its own specific timeline that functions differently from a standard personal injury claim. These are not exactly "extensions" but separate statutes with unique starting points and durations. It is critical to understand these specific deadlines, and you can learn more by reading about the statute of limitations for wrongful death.

Ultimately, both tolling and equitable estoppel are complex legal doctrines that depend on the specific facts of a case. They serve as a reminder that while the statute of limitations for insurance claims is a strict rule, the legal system has safeguards intended to ensure fairness. It’s why understanding the deadline—and all the potential exceptions—is very important.

Practical Steps to Protect Your Claim Timeline

Navigating the legal deadlines for an insurance claim can feel overwhelming. But there are straightforward, practical things you can do to protect your rights and keep your claim on solid ground.

From the moment an incident happens, it is helpful to start building a record. These are not complicated legal tactics; they are good habits that create a clear, organized file. Getting this right from the start can make a difference down the road.

Immediately Document Everything

In the aftermath of an injury or accident, details can become less clear over time. That's why a good first step is to document everything possible while the memory is fresh. This initial evidence is often very powerful.

Get a dedicated folder—digital or physical—and start collecting information.

- Photographs and Videos: Use your phone to take extensive photos of the scene, property damage, and any visible injuries. Shoot from different angles and distances. A short video can capture context that a still image might miss.

- Witness Information: If anyone else was present, getting their name and phone number can be helpful. A third-party account can be valuable.

- Official Reports: Always request a copy of the police report or any other official incident report. This is a foundational piece of a claim.

This simple act creates a crucial snapshot of the event before time can blur the facts.

Report the Incident Promptly

Your insurance policy is a contract, and nearly every contract requires you to notify the insurer of a potential claim in a timely manner. Do not delay. Reporting the incident as soon as possible officially starts the claims process and creates a record that you have held up your end of the agreement.

This first call is a critical step. It establishes the date the insurance company was put on notice, a key milestone in a claim's timeline. As with all legal agreements, understanding the terms is important, which is why experts emphasize effective contract management practices. It is a good practice to write down who you spoke to, the date and time, and your claim number.

Maintain Thorough Records

As a claim moves forward, staying organized becomes very helpful. This is about more than just the initial evidence; it means tracking every single interaction and piece of paper that comes your way.

A well-organized file is more than just a collection of papers; it's a clear, chronological story of your claim. It allows you to track progress, reference past communications, and ensure no important detail is overlooked.

Keep a running log of every phone call with adjusters—note the date, time, and a summary of the conversation. Save all emails and letters in your dedicated folder. This creates a history of your communications with the insurance company. If you're preparing for these discussions, looking at a demand letter template can provide a general idea of how to present a claim formally.

Finally, be meticulous about collecting all related expenses. This includes medical bills, co-pays, pharmacy receipts, and proof of any other out-of-pocket costs. This paper trail is the evidence used to demonstrate the value of a claim.

Common Questions About Oregon Insurance Claim Deadlines

When you're dealing with an insurance claim, the last thing you want to worry about is a legal technicality like the statute of limitations. But these deadlines are incredibly important, and misunderstanding them can have serious consequences.

Let's walk through some of the questions we hear most often. These answers are designed to give you a solid, foundational understanding, but remember, they aren't a substitute for legal advice on your specific case.

What Happens If I Miss the Statute of Limitations for My Insurance Claim in Oregon?

Generally, if you miss the deadline, your right to sue could be lost. A court may permanently dismiss your case, meaning you have lost the opportunity to pursue it in the legal system.

This can be a difficult outcome, but it can happen regardless of the strength of a case. It is one of the main reasons why paying close attention to these timelines is critical from day one. How the rule gets applied depends on the specific facts of a situation.

Does Negotiating with an Insurance Adjuster Pause the Statute of Limitations?

This is a common and potentially risky assumption. In most cases, talking or negotiating with an insurance adjuster does not stop the clock on your statute of limitations. That legal deadline continues to run in the background, regardless of your conversations.

To officially pause the deadline, a formal written contract called a "tolling agreement" signed by both sides may be required. This area of law can be complex, and what is said (or not said) during negotiations can become very important later on.

Do not mistake negotiation for legal action. The statute of limitations is a hard legal deadline. Only filing a formal lawsuit with the court will officially stop the clock.

If My Child Was Injured Is the Deadline Different?

Yes, cases involving minors often operate under special rules. The law recognizes that minors cannot file lawsuits for themselves, so in Oregon, the statute of limitations is often "tolled" (paused).

For many types of claims, this pause can last until the child turns 18, which can extend the window for filing a lawsuit. However, the laws in this area are very specific and have their own exceptions, so one should not rely on the general principle alone. It is always best to get clear information based on a child's specific circumstances.

Is the Deadline for Filing an Insurance Claim the Same as the Deadline for Filing a Lawsuit?

No, and confusing the two is a major potential pitfall. You are dealing with two separate and different timelines.

- Your Policy Deadline: This is the timeline written into your insurance contract. It dictates how long you have to notify the company of a loss and submit your paperwork (like a Proof of Loss form).

- The Statute of Limitations: This is the deadline set by Oregon state law that controls how long you have to file a lawsuit in court.

You could do everything correctly according to your insurance policy—reporting the claim on time, cooperating fully—but still lose your right to sue if the legal deadline passes while you're negotiating. This is a critical distinction to keep in mind.

Understanding these deadlines is the first step, but applying them to your situation requires careful analysis. If you have questions about your auto accident, workers' compensation, or Social Security Disability claim, the team at Bell Law is here to help. Contact us for guidance on your next steps at https://www.belllawoffices.com.

Disclaimer: The information on this page is provided for general informational purposes only and is not legal advice. Reading this content does not create an attorney-client relationship. For advice about your specific situation, please contact a licensed attorney.