What Is a Typical Rear End Collision Settlement in Oregon?

"I was satisfied once John Bell took over my case."

"Communication was always timely."

What Is a Typical Rear End Collision Settlement in Oregon?

If you've been rear-ended, one of the first questions on your mind is probably, "What is my case worth?" It’s a completely fair question, but the answer isn't a simple number.

For minor to moderate injuries, a typical rear-end collision settlement in Oregon can land anywhere between $10,000 and $75,000. Of course, for devastating or life-altering injuries, that figure can climb much, much higher. The key takeaway is that there's no magic formula; the final value is built from the specific, unique details of your accident.

Understanding What Your Settlement is Actually Made Of

Trying to pin down a "typical" settlement value is like asking the price of a "typical" house. Is it a one-bedroom condo or a five-bedroom estate? The value depends entirely on what it’s made of. The same is true for your injury claim.

Your settlement isn't just one lump sum. Instead, it’s a carefully calculated total that accounts for every single loss you've suffered. Each piece—the ER visit, the physical therapy sessions, the wages you lost while recovering, and the daily pain you've had to endure—is a building block. Only when we assemble all these blocks can we see what your claim is truly worth.

In this guide, we'll walk through exactly how those pieces come together. We'll cover:

- The key components that drive the value of your claim.

- Factors that can dramatically increase or decrease your final settlement.

- A few real-world scenarios to show how this plays out.

- Common insurance company tactics and how to counter them.

To give you a general idea, settlements for minor soft-tissue injuries like whiplash often settle in the $10,000 to $25,000 range. When injuries are more serious—think herniated discs or significant time off work—settlements more commonly fall between $25,000 and $75,000. Data from across the legal industry shows that the median recovery for auto injury cases often lands in the $25,000 to $55,000 range, which makes sense given how many claims fall into that moderate category. You can learn more about how these average payouts are calculated from legal market reports.

A settlement isn't a prize—it's compensation. It's a figure calculated to cover every single loss you’ve had and will have because of the crash. The goal is to make you whole again, at least from a financial standpoint.

Ultimately, things like your specific injuries, the evidence we can gather, and even the county where the crash happened will all play a part. Getting a handle on these factors from the start is the best way to set realistic expectations for the process ahead.

Quick Guide to Rear-End Settlement Ranges

While every case is unique, it can be helpful to see some general ranges based on the severity of the injuries involved. This table provides a bird's-eye view to help set expectations.

| Minor | Soft tissue sprains (whiplash), minor bruising, short-term pain. | $10,000 - $25,000 |

| Moderate | Herniated discs, concussions, simple fractures, longer recovery. | $25,000 - $75,000 |

| Severe | Spinal cord injuries, traumatic brain injuries (TBI), complex fractures, surgery required. | $100,000+ |

| Catastrophic | Permanent disability, paralysis, life-altering disfigurement. | $500,000 - Millions |

Remember, these are just ballpark figures. A "minor" injury with complications could be worth more, while a "severe" case with weak evidence might settle for less. This is why a detailed evaluation of your specific situation is so critical.

The Core Components of Your Claim Value

Trying to figure out what a rear-end collision settlement is worth can feel a bit like putting a puzzle together. You have a lot of different pieces, and each one plays a role in forming the final picture. In legal terms, these pieces are called "damages," and they fall into two main categories: economic and non-economic.

Getting a handle on both is the key to understanding what a fair offer truly looks like.

Economic Damages: The Tangible Costs

Let’s start with the easy part. Economic damages are all the concrete, out-of-pocket expenses and financial losses you've suffered because of the crash. If you have a bill, a pay stub, or a receipt for it, it almost certainly counts as an economic damage.

Think of these as the solid, provable foundation of your claim. This is why keeping a detailed file of every expense is so important—it’s the hard evidence of your financial losses.

Here’s what typically falls under this umbrella:

- Medical Expenses: This is a big one. It includes the ambulance ride, the ER visit, doctor's appointments, chiropractic care, physical therapy, medications, and any medical equipment you might need.

- Lost Wages: If you couldn't work because of your injuries, you're owed that lost income. This isn't just for salaried employees; it also covers missed hourly wages, lost commissions, and even canceled gig work.

- Future Medical Care: A serious injury doesn't just go away when the initial treatment is over. Your settlement needs to account for the cost of future needs, like ongoing physical therapy, potential surgeries, or long-term pain management.

- Vehicle Repair or Replacement: Pretty straightforward—this is what it costs to either fix your car or, if it’s totaled, what its fair market value was right before the accident.

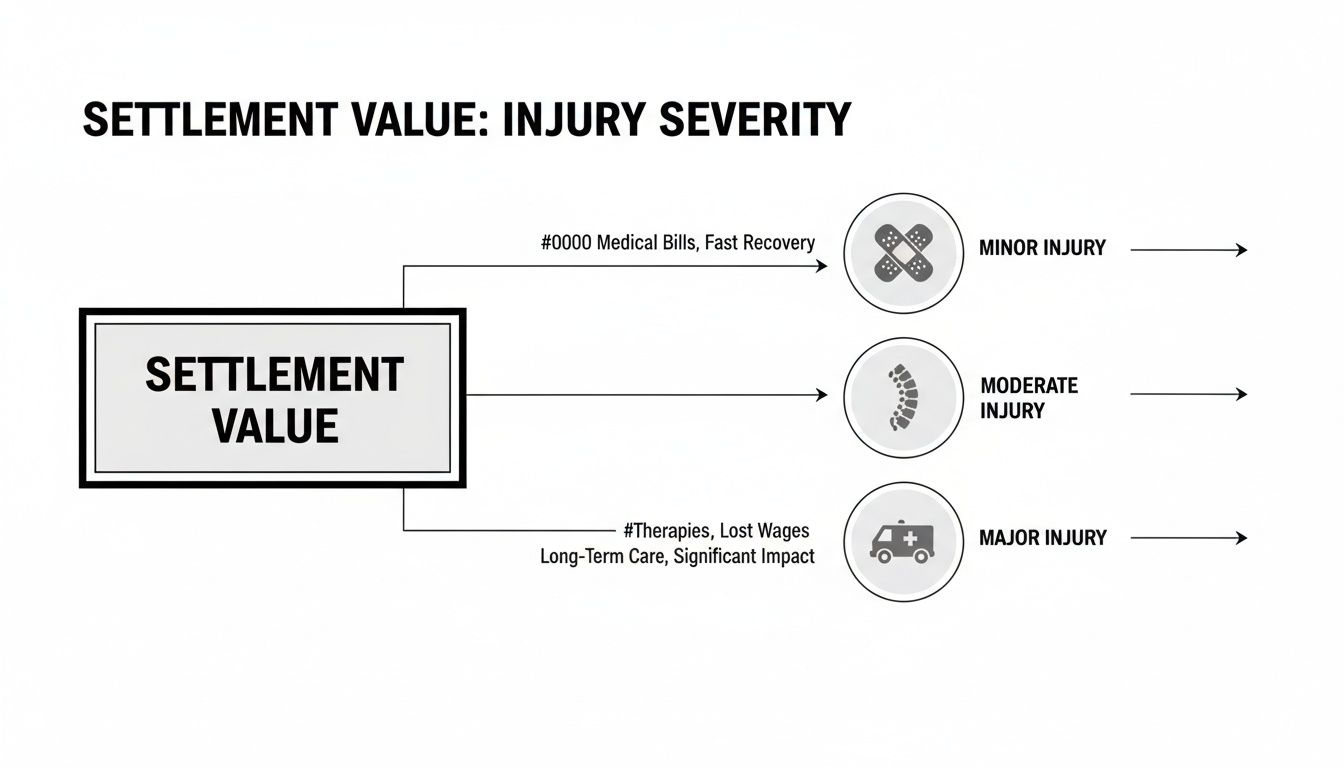

This diagram helps visualize how the value of these components grows as injuries become more severe.

As you can see, a claim's value scales directly with the seriousness of the injuries and the level of medical care required. Knowing the potential costs of treatments, like non-surgical disc herniation treatment, is a crucial part of building an accurate valuation.

Non-Economic Damages: The Human Cost

Now for the less straightforward part. While economic damages cover the money you've lost, non-economic damages are meant to compensate for the human toll of the accident. These are very real losses, but they don't come with a neat price tag.

How much is chronic pain worth? What's the value of not being able to pick up your kids or go for a run anymore? This is where things get more subjective, and it’s often the most contentious part of a negotiation.

To put a number on it, insurance companies and lawyers often use a "multiplier" approach. They'll take your total economic damages and multiply them by a number, typically between 1.5 and 5, depending on how significantly the accident has impacted your life.

Pain and suffering isn't just about physical discomfort. It includes the emotional distress, anxiety, sleep loss, and the overall reduction in your quality of life that results from the collision.

Figuring out this part of your claim is where having an experienced advocate makes all the difference. A minor whiplash that resolves in a few weeks might get a low multiplier. But a severe injury that leads to surgery and permanent limitations will justify a much, much higher one. To get a better feel for this, you can read our guide on how much pain and suffering is worth.

What Factors Really Drive Your Settlement Amount?

When you’re trying to figure out what a typical rear-end settlement looks like, it’s tempting to search for a simple number. But the truth is, there’s no magic formula. Think of your initial damages—your medical bills and lost wages—as the starting point. From there, a handful of critical factors will either drive your final settlement number up or push it down.

What you really need to understand are the specific strengths and weaknesses of your case. Two crashes that look identical on the surface can end up with vastly different settlement amounts because of these key details. Let’s walk through the exact things insurance companies and attorneys look at when they put a number on a claim.

Who Was at Fault? A Look at Oregon’s Negligence Law

In a rear-end collision, it's usually a safe bet that the driver who hit you from behind is at fault. It’s one of the few semi-clear-cut rules in traffic law. But "usually" isn't "always." What if the driver in front of you had broken brake lights? Or what if they slammed on their brakes for no reason at all? Suddenly, things get more complicated.

This is where Oregon's modified comparative negligence rule comes into play. It’s a legal way of saying that fault can be shared. If you’re found to be partially responsible for the crash, your settlement is reduced by your percentage of fault.

Here's a real-world example: Let's say your total damages add up to $50,000. If it’s determined that you were 10% at fault, your final recovery gets cut by $5,000, leaving you with $45,000. But here’s the crucial part: if you are found to be 51% or more at fault, you can’t recover a single dollar in Oregon.

The Story Your Medical Records Tell

Without a doubt, the seriousness of your injuries is the single biggest factor determining your case's value. A collision that results in a herniated disc and a recommendation for surgery is in a completely different league than a minor whiplash case that clears up after a few weeks of physical therapy.

Your medical records are the proof. They are the official story of what this accident did to your body. If you delay getting treatment or have big, unexplained gaps in your physical therapy, you're handing the insurance adjuster a reason to argue your injuries aren't that bad or weren't caused by the crash. Clear, consistent, and detailed medical documentation is the bedrock of a strong claim.

The Reality of Insurance Policy Limits

This is a tough one, and it’s a reality that can be incredibly frustrating for injured people. You can have a rock-solid case that is legitimately worth $200,000, but if the person who hit you only carries Oregon's minimum bodily injury liability coverage of $25,000 per person, that's all their insurance company is going to pay. They legally don't have to pay a penny more.

This is exactly why your own insurance policy is so important. Your Uninsured/Underinsured Motorist (UIM) coverage is designed for this exact scenario. If the at-fault driver's policy is too small to cover your damages, you can file a UIM claim with your own insurance company to make up the difference, right up to the limits of your own policy.

Factors Influencing Your Settlement Amount

It can be helpful to see these concepts laid out side-by-side. The table below shows how the very same factors can either build up your case or chip away at its value.

| Liability | The other driver is clearly 100% at fault, confirmed by a police report and witnesses. | You are found partially at fault (e.g., you had a broken taillight). |

| Medical Proof | You sought immediate medical care and followed all doctor's orders consistently. | There are long gaps in your medical treatment or you delayed seeing a doctor. |

| Injury Type | Objective injuries are present (e.g., a fracture or herniated disc visible on an MRI). | Injuries are subjective "soft tissue" claims with little objective proof. |

| Pre-Existing Issues | The crash clearly caused a new injury, documented by medical experts. | You had a pre-existing condition in the same area and records are unclear on aggravation. |

As you can see, the final settlement is a balancing act. The more factors you have in the "Positive Impact" column, the stronger your negotiating position will be.

Real-World Settlement Scenarios

It’s one thing to talk about "economic damages" and "pain and suffering" as concepts. It’s another to see how they actually play out in a real person's life. To make this tangible, let's walk through three different—but very common—hypothetical scenarios.

Each story shows how the specific details of an injury, recovery time, and the impact on daily life come together to shape the final settlement amount.

Keep in mind, these are just illustrations. For an estimate tailored to your own situation, our car accident compensation calculator can give you a much clearer picture.

Scenario 1: The Minor Whiplash Case

Maria is waiting in traffic when another driver bumps into her from behind. It wasn't a hard hit, and the damage to her car is minor, but she feels her neck stiffen up almost immediately. She does the right thing and heads to an urgent care clinic that same day, where she’s diagnosed with minor whiplash.

Her doctor prescribes six weeks of physical therapy, which she diligently completes. The injury caused her to miss two days of work right after the accident, but she made a full recovery.

- Economic Damages:

- Medical Bills: $3,500 (Urgent care visit plus all physical therapy sessions)

- Lost Wages: $400 (Two days of missed work)

- Total Economic Damages: $3,900

- Non-Economic Damages: Because Maria’s recovery was relatively quick and she had no lasting issues, a lower pain and suffering multiplier (around 2.0x) is appropriate. This adds $7,800 to her claim.

Potential Settlement Range: $11,000 - $13,000. This is a fairly typical outcome for a straightforward soft-tissue injury case where the treatment is documented and the recovery is complete.

Scenario 2: The Moderate Herniated Disc

David gets rear-ended at a stoplight, and this time, the impact is significant. He feels a sharp, shooting pain in his lower back. An MRI later confirms what he feared: a herniated disc. His doctor recommends holding off on surgery, instead creating a treatment plan with chiropractic care and pain management injections.

As a construction worker, David can’t perform his usual duties. He’s put on light duty for three months, which means a noticeable cut in his pay. The nagging, constant pain also messes with his sleep and keeps him from hiking and fishing on the weekends.

- Economic Damages:

- Medical Bills: $15,000 (ER visit, MRI, specialists, injections, and therapy)

- Lost Wages/Reduced Earnings: $8,000

- Total Economic Damages: $23,000

- Non-Economic Damages: This is a much more serious injury. The recovery is longer and it’s had a real effect on his quality of life. A moderate multiplier (around 3.0x) is justified here, bringing the pain and suffering component to $69,000.

Potential Settlement Range: $85,000 - $95,000. The higher value reflects an objective injury confirmed by an MRI and the significant disruption to David’s work and personal life.

Scenario 3: The Severe Surgical Case

Sarah is on the freeway when she is hit from behind at high speed. The impact is catastrophic, shattering her ankle. She’s rushed to the hospital for emergency surgery, where doctors use plates and screws to piece the bone back together.

She spends several days in the hospital and can't return to work for a full six months. Her doctors are frank: she will probably develop arthritis in that ankle and will likely have a permanent limp. This life-altering injury means she can no longer continue in her career.

This is where a case becomes much more complex. We aren't just calculating past bills; we have to project future damages. A skilled attorney will bring in medical and vocational experts to forecast the costs of future care and her lost earning capacity over a lifetime.

- Economic Damages:

- Past Medical Bills: $85,000

- Past Lost Wages: $30,000

- Projected Future Medical Costs: $50,000

- Projected Lost Earning Capacity: $250,000

- Total Economic Damages: $415,000

- Non-Economic Damages: Given the permanent, life-changing nature of her injury, a high multiplier ( 4.0x or even more) is absolutely warranted.

Potential Settlement Range: $1,000,000+. When an accident causes this level of permanent harm, settlements frequently reach seven figures to truly account for the lifelong physical, emotional, and financial toll on the victim.

Navigating Insurer Tactics and the Settlement Timeline

After a collision, all you want is to get things resolved and move on. It’s completely understandable. But when it comes to getting a fair rear end collision settlement, think of it more like a marathon than a sprint. The process isn't quick for a reason: it takes time to figure out the full extent of your injuries and what this crash has truly cost you.

Everything hinges on a concept called Maximum Medical Improvement (MMI). This is simply the point when your doctor says you've recovered as much as you're going to. Reaching MMI is a huge milestone. Before you hit that point, you have no real idea what your final medical bills will look like or if you’ll be left with any permanent issues. Settling before MMI is a massive risk, and it’s a gamble that insurance companies are more than happy for you to take.

Understanding the Timeline

So, how long does this all take? It really depends. Most rear-end collision claims get resolved somewhere between 6 months and 3 years, but the most common window is around 12–24 months. This timeline gives you the space needed for a proper diagnosis, a full course of treatment like physical therapy, and a clear picture of any long-term effects.

Sure, a minor fender-bender might settle faster. But cases involving serious injuries or surgery can easily stretch beyond 36 months. The main reason for the wait is simple: you have to document your entire recovery journey to prove the value of your claim.

Common Insurance Adjuster Tactics

Let’s be clear about one thing: insurance adjusters are skilled negotiators. Their job isn’t to help you; it’s to protect their company’s profits by paying out as little as possible. Knowing their playbook is your best defense.

You'll almost certainly run into a few of these common tactics:

- The Quick, Lowball Offer: You might get a call within days of the crash from an adjuster offering a fast check to "get this all behind you." This isn't a gesture of goodwill. It's a calculated strategy to get you to settle before you even know how badly you’re hurt.

- Requesting a Recorded Statement: They’ll tell you it’s just “standard procedure,” but the real goal is to get you on record. They are listening for any little inconsistency or admission—anything they can twist and use to devalue your claim later on.

- Disputing Your Medical Treatment: Don't be surprised if the adjuster starts playing doctor. They might question why you need so much physical therapy or try to blame your pain on a pre-existing condition they found in your old medical files.

Key Takeaway: The insurance adjuster is not your friend. Their goal is to close your case for the lowest amount possible. Never accept the first offer, give a recorded statement, or sign anything without talking to a lawyer first.

Fighting back against these tactics means being strategic. Politely but firmly decline any quick settlement offers and requests for a recorded statement. The single most important thing you can do is follow your doctor's treatment plan perfectly—this builds a rock-solid medical record that’s hard to argue with.

Knowing how to deal with insurance adjusters is a crucial part of the process and helps level the playing field. When you have an experienced attorney handling these conversations for you, you can rest assured that your rights are being protected every step of the way.

Why an Attorney Is Your Strongest Advocate

Trying to navigate a rear-end collision claim by yourself is a bit like stepping into the ring against a professional boxer. You might land a punch or two, but you’re up against an opponent who does this for a living. Going it alone almost always means leaving money on the table.

An experienced personal injury attorney is much more than a paperwork filer; they’re your strategist, your shield, and your champion. Their job is to build a case that tells the complete story of your accident and its impact on your life, capturing not just the obvious costs like medical bills but also projecting future expenses you might not even think of. They take over the evidence gathering, handle every frustrating phone call with the insurance company, and fight for you at the negotiating table.

Leveling the Playing Field

Insurance companies are masters at one thing: minimizing what they pay out. It’s their business model. This is especially true for rear-end crashes, which are incredibly common—making up 25%–28% of all police-reported accidents. Because of this high volume, insurers often try to clear these cases quickly with lowball offers before victims understand the true value of their claim. You can read more about how crash frequency shapes settlement tactics in other industry deep dives.

But how can you afford an expert to fight for you? This is where the system is designed to help.

Personal injury attorneys work on a contingency fee basis. This means you pay absolutely nothing upfront. The attorney’s fee is simply a percentage of the money they recover for you. If they don’t win your case, you don’t owe them a dime.

This setup is a game-changer. It gives you immediate access to top-tier legal help without any financial risk. More importantly, it means your attorney is just as invested in getting you the best possible outcome as you are. Their success is literally tied to yours, ensuring you have a dedicated advocate fighting for a fair typical rear end collision settlement against a powerful insurance company.

Your Questions Answered

When you've been in a rear-end accident, questions start piling up fast. Here are some straightforward answers to the things we hear most often from clients in Oregon.

How Long Do I Have to File a Personal Injury Claim in Oregon?

In Oregon, the clock is ticking from the moment of the crash. You generally have two years to file a personal injury claim. This is known as the statute of limitations.

It sounds like a long time, but it can fly by. If you miss this two-year deadline, you almost always lose the right to seek compensation for your injuries, no matter how strong your case is.

Is My Case Going to End Up in Court?

Probably not. The reality is that the vast majority of car accident claims—well over 90% of them—settle out of court.

Going to trial is expensive and unpredictable for everyone, including the insurance company. We typically only file a lawsuit when an insurer digs in their heels and refuses to negotiate fairly. It's a strategic move to show them we mean business and get them back to the table.

Filing a lawsuit is a tool, not the goal. The goal is always to get you the compensation you deserve. Sometimes, taking that step is what it takes to make an insurance company pay attention and offer a fair settlement.

The Insurance Company Made an Offer. Should I Take It?

My advice is almost always no, especially if it's their first offer. That initial number is a starting point, and it's intentionally low.

Insurance adjusters are trained to get you to accept a quick, cheap payout before you realize the true cost of your injuries. They're counting on you wanting to put this all behind you. But that first offer rarely covers things like future physical therapy, long-term pain, or the full impact the accident has had on your life.

What Happens if the Other Driver Doesn't Have Insurance?

This is a scary situation, but you still have options. If the driver who hit you was uninsured or fled the scene, you can turn to your own insurance policy, as long as you have Uninsured/Underinsured Motorist (UM/UIM) coverage.

This is exactly why this type of coverage exists—to protect you from irresponsible drivers. An experienced attorney can help you file a UM/UIM claim and make sure your own insurance company treats you fairly.

Feeling overwhelmed by the claims process is completely normal. But you don’t have to handle it by yourself. The team at Bell Law is here to cut through the confusion and fight for the compensation you are owed.

If you have more questions or are ready to discuss your case, reach out to us for a free, no-pressure consultation. Find out how we can help at our Bell Law offices website.

Disclaimer: The information on this page is provided for general informational purposes only and is not legal advice. Reading this content does not create an attorney-client relationship. For advice about your specific situation, please contact a licensed attorney.